Gainfully employed but struggling with bank mortgage approval? WVOE mortgage loans offer a solution, even without tax returns or W-2s. Ideal for those with complex financial profiles, these loans use bank statements and employment verification for approval, bypassing traditional documentation requirements. This opens doors to non-bank lenders, offering flexibility beyond conventional financing constraints.

WVOE mortgage loans: Simplifying employment verification

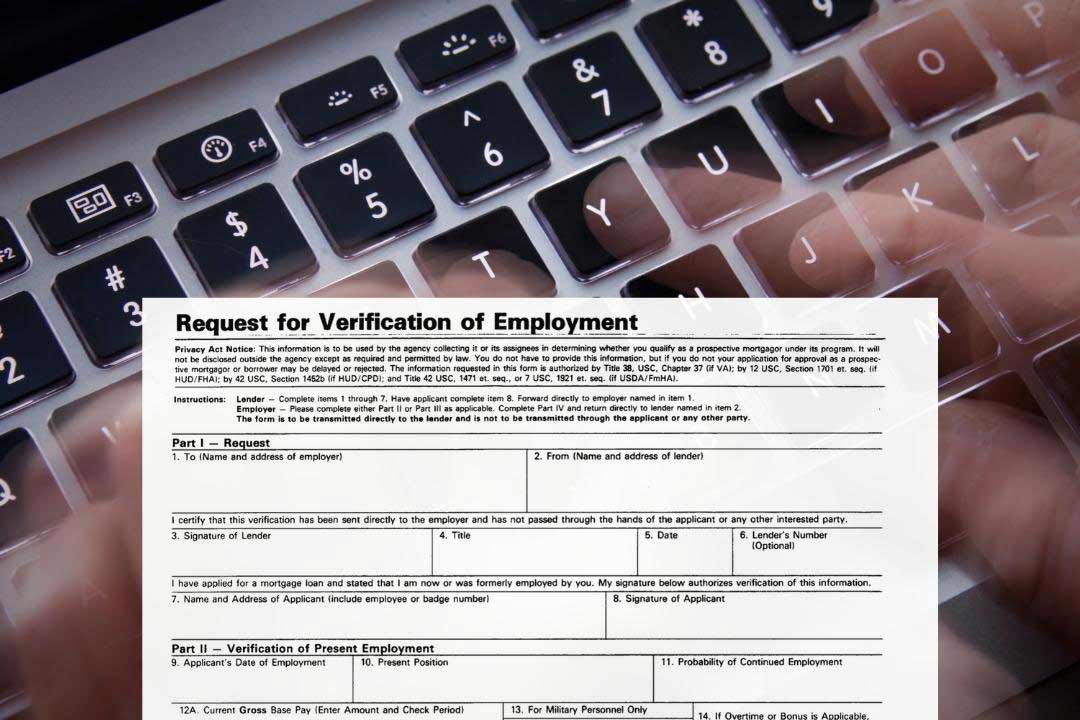

This program requires a written verification of employment, over and above any self-employment income you may be able to document. The lender will send your employer a Form 1005, which asks them to verify specific details of your employment. These include your compensation, how it’s structured (salary, bonuses, commissions, etc.), date of hire and a summary of year-to-date earnings.

The form must be filled out by an officer of your company or an HR/payroll representative. You won’t handle this form yourself: This communication occurs directly between the lender and your employer.

Lenders will compare your personal bank statement with the data inputted by your employer into the form to make sure the two are consistent with one another and your other statements regarding your income. They’ll also conduct an Internet search of the business to verify its existence.

This particular loan program is designed for borrowers who can prove employment. It isn’t specifically designed for self-employed borrowers since it relies on a written income verification from your employer. However, there are some great mortgage options out there for the self-employed and independent contractors/1099 workers and gig economy workers as well.

Ideal candidates for WVOE mortgage loans

WVOE mortgage loans offer innovative solutions for borrowers who lack traditional tax returns, providing a pathway to homeownership based on employment verification. For example, some borrowers have very high deductions that artificially reduce their income. It’s also a good solution for borrowers who haven’t filed tax returns in years.

Furthermore, WVOE loans can often close much quicker than full-documentation loans with traditional underwriting – especially if your tax or income situation is complicated.

Getting approved: Navigating WVOE mortgage loan process

Under WVOE mortgage programs, lenders look primarily at your income and your credit history. o qualify for WVOE mortgage loans, borrowers need a FICO score of 660 or higher, in addition to verifiable income.

You’ll also need to submit at least one monthly bank statement showing deposits consistent with your claimed income.

Lenders will also check with your existing landlord or mortgage company: You need to have no late rent or mortgage payments for at least 24 months to be competitive.

Your employer can’t be a family member or other related individual.

Only wage/salary income (i.e., base pay, overtime, commissions, bonuses) is counted under this program. Supplemental sources of incomes such as rental income aren’t countable under a WVOE program.

If you need to include other sources of income to qualify, or you want to purchase an investment property, contact us about our other residential mortgage alternatives.

Case study: Getting a WVOE mortgage despite a period of unemployment

Here’s a good example from our own practice of how a WVOE program works, and how flexible and creative lenders in the non-QM space can be:

One woman came to us after being denied by another lender. She was under contract to purchase a condominium, and her closing deadline was approaching. We saw right away that she had several issues, beginning with her work history: Lenders normally require applicants to have worked at least 24 months with the same employer.

But our client had recently received a cancer diagnosis, which forced her to take 10 months off for treatment. She was finally medically cleared to return to work 14 months prior to her application. She returned to work in the same line of business. But she couldn’t satisfy the normal 24-month work history requirement.

She was also trying to buy a non-warrantable condominium in a project where the HOA had brought a construction defect lawsuit against the developer. Condos with pending construction defect claims are more difficult to finance because they are riskier for lenders, and don’t qualify for conventional bank financing from qualifying mortgage lenders. (Click here for more information on getting a mortgage on properties with pending construction defect claims.)

The condo development was also 66% rentals, rather than owner-occupants, which was another factor making the property difficult to finance.

Furthermore, because of the lengthy period of unemployment, her tax returns didn’t show enough income over the previous two years to qualify for a mortgage. We knew we needed to use a WVOE so that the tax returns wouldn’t be an issue.

Applying the “Five Cs” to get the loan approved

So we knew our work was cut out for us: Our client had issues with several of the Five Cs that mortgage lenders look at to assess loan applications:

- Character

- Capacity

- Capital

- Conditions

- Collateral

We knew character wouldn’t be an issue. Market conditions were acceptable. But because of her reduced income over the previous two years and the period of unemployment, we had to overcome a hurdle when it came to demonstrating her capacity to cover her mortgage payments in the future.

She wasn’t sitting on a huge pile of assets, so she wasn’t strong in the capital column. And because of the high renter occupancy and the pending construction defect litigation, there were serious problems with the collateral on this loan.

We knew of a lender who would likely be flexible and be able to look at the totality of our client’s situation. We completed the application with the client, and the client also attached a detailed letter explaining the reason for her break in employment.

In addition to explaining her period of unemployment, our client was also able to show that she had a JD degree and had over 15 years of gainful employment experience as an estate planning attorney and had ample earning capacity to cover her mortgage payments.

Also in the plus column, our client had a high credit score of 766. She also had relatively little debt, so her credit utilization ratio was strong at 36%. Each of these helped buttress her capacity to make her payments.

Because we were dealing with a non-bank lender in the non-QM mortgage industry, they weren’t beholden to Fannie and Freddie’s bureaucratic requirements. They were able to recognize the quality of the borrower and granted several exceptions to their usual underwriting standards.

The lender approved her application for 80% LTV. And we got a clear-to-close in just 14 business days – well ahead of her closing deadline.

Can I refinance using a WVOE mortgage?

Yes, you can use a written verification of employment to help you qualify for either a purchase or refinance of your primary residence. In either case, you can qualify without providing tax returns, W-2s, or 1099s. Just a good credit history (FICO 660 or better), a completed Form 1005 from your employer, and at least one month’s bank statements covering a full 30 days.

If you refinance to get cash out, you may be able to have the cash-out proceeds credited towards required reserves.

How much can I borrow with a WVOE mortgage?

The maximum amount you can borrow under this program is 80% LTV for purchase and rate-and-term refinances. The maximum you can borrow in a cash-out refinance is 75% LTV.

What properties qualify?

At present, WVOE programs will only finance the buyer’s own personal primary residence. However, if you want to buy an investment property, vacation home, or short-term rental property, there are several other terrific and flexible programs you can still use without necessarily needing to submit tax returns, W-2s, or 1099s.

For example, you can purchase any of these properties using a debt service coverage ratio (DSCR) lending program, or using one of several bank statement loan programs that require 1 to 2 years of consecutive bank statements and/or a verification of your income from your tax preparer.

Conclusion

Programs like written verification of employment loans, bank statement loans, and no-ratio programs exemplify the flexibility and creativity of alternative lenders in the non-bank, non-QM space.

At DAK Mortgage, we have a particular focus on special circumstances.

Even if you have years of unfiled tax returns, or you have gaps in your employment history, or credit problems, don’t be discouraged. Even if bank lenders have turned you down, chances are excellent that we can find a mortgage program that suits your needs, helps you refinance to better terms or a lower payment, or even purchase your dream home.

Contact us today, and let’s discuss your situation.

We look forward to working with you.